JOHN CHIANG

CALIFORNIA STATE TREASURER

CALIFORNIA BONDS: 101

A Citizen’s Guide to

General Obligation

Bonds

2016 EDITION

1

Q. What is a municipal bond?

A. A bond is a loan. ere are many types of municipal bonds, but they have

only one purpose – to borrow money. It involves a promise to pay money,

with interest, on a specied date.

SECTION 1 BONDS 101: Q&A

Q&A

Q. Who uses them?

A. e state and many local governments, especially school districts.

Q. What types of municipal bonds are there?

A. e two types most pertinent to public nance are revenue bonds and

general obligation (GO) bonds. To repay investors, revenue bonds rely on

monies derived from the sale of commodities (such as water) or from the use

of facilities (such as airports).

State general obligation bonds enjoy the “full faith and credit” of California.

“Full faith and credit” expresses the commitment of the issuer to repay the

bonds from all legally available funds. GO bonds issued by local governments,

such as schools, are often only payable from the local issuer’s property taxes.

is guide will focus on general obligation bonds. Future publications will

address other forms of government debt.

2

Q&A

Q. Do GO bonds require voter approval?

A. Yes. State GO bonds require majority voter approval. Locally issued GO bonds

require 2/3 voter approval. However, GO bonds by schools can be issued with

55% voter approval if certain statutory requirements are met.

Q. What are GO bonds used for?

A. ey are primarily used to nance infrastructure projects, including roads,

bridges, water and sewer facilities, levees, K-14 schools, public universities and

other critical public works projects.

Q. How do bonds dier from a loan?

A. e capital market has a dierent set of expectations than bank lenders have.

Primarily, these expectations relate to the certainty of repayment, a more limit-

ed tolerance for variances in nancial condition, and the size of the loan.

Also, publicly oered bonds are subject to federal securities fraud laws and

require a very high level of caution about what is disclosed and when it is dis-

closed.

Q. What is the total amount of outstanding State of California

issued GO bonds?

A. $74.9 Billion**

Q. What is the total amount of State of California GO bonds

authorized but not yet issued?

A. $27.6 Billion**

*Source: Securities Industry and Financial Markets Association

**As of June 30, 2016

Moody’s Standard & Poor’s Fitch

Current Aa3 AA- AA-

2009

Baa1* A** BBB*

3

A bond credit rating is similar to an individual’s credit score.

e better the credit rating, the cheaper the borrowing cost.

California’s credit rating has improved dramatically since the Great Recession.

On August 12, 2016, Fitch Ratings upgraded California’s GO credit rating

one notch to AA-, elevating the state to the “high grade” category.

Moody’s and S&P have maintained their Aa3 and AA- ratings respectively.

SECTION 2 THE RATINGS GAME

Moody’s Standard & Poor’s Fitch The Ratings Map

Aaa AAA AAA

High Grade

Aa1 AA+ AA+

Aa2 AA AA

Aa3 AA- AA-

A1 A+ A+

Upper Medium GradeA2 A A

A3 A- A-

Baa1 BBB+ BBB+

Lower Medium Grade

Baa2 BBB BBB

Baa3 BBB- BBB-

Ba1 BB+ BB+

Speculative Ba2 BB BB

Ba3 BB- BB-

B1 B+ B+

Highly SpeculativeB2 B B

B3 B- B-

Caa1 CCC+ CCC Substantial Risks

Caa2 CCC Extremely Speculative

Caa3 CCC-

Default

Ca CC

D DDD

DD

D

*Credit rating as of July 2009

**Credit rating as of February 2009

Investment GradeNon-Investment Grade

4

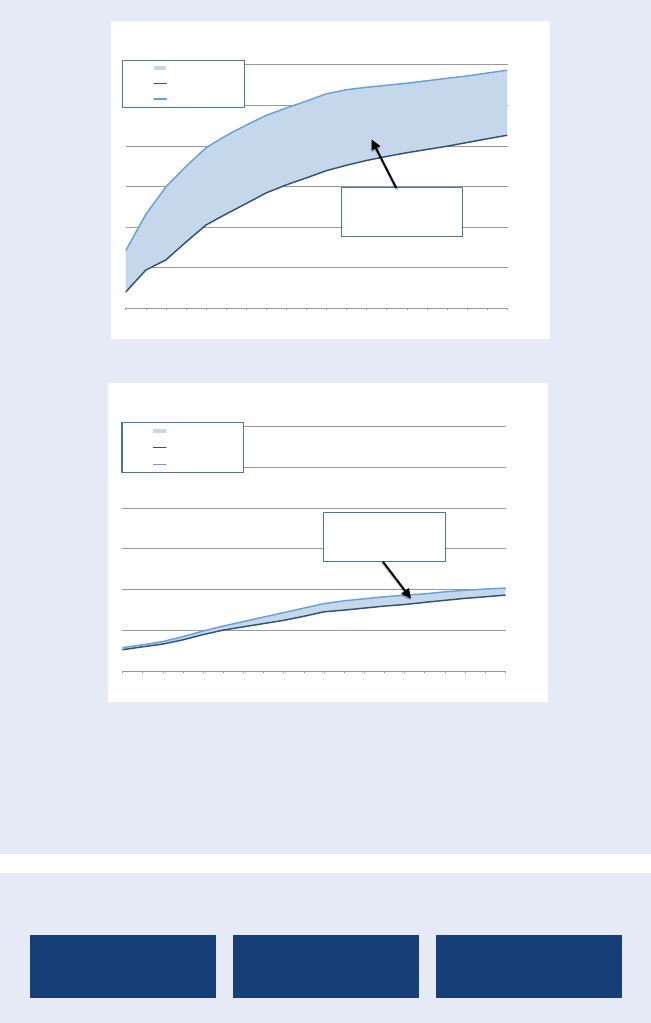

Higher credit ratings produce lower borrowing costs and taxpayer savings.

For example, the next two charts demonstrate how much taxpayers

can save when ratings go up.

Three Major Factors Rating Agencies Review When Grading

California’s Credit Worthiness

Economy

Financial Operations

and Results

Management

COST TO CA COMPARED TO AAA-RATED ISSUER:

Then - $201.6 Million • Now - $12.2 Million

Savings = $189.4 Million Per $1 Billion Borrowed

Source: Municipal Market Data as of 7/1/09

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

1yrs 2yrs 3yrs 4yrs 5yrs 6yrs 7yrs 8yrs 9yrs 10yrs 11yrs 12yrs 13yrs 14yrs 15yrs 16yrs 17yrs 18yrs 19yrs 20yrs

InterestRate

LengthofBorrowing

COMPARING CALIFORNIA'S BORROWING COSTS TO AAA-RATED ISSUER

(as of 7/1/2009)

DIFFERENTIAL

AAA ISSUER

CALIFORNIA

For each $1.0 billion borrowed,

California would have paid $201.6

million more over a 20-year period than

a AAA-rated issuer paid.

Source: Municipal Market Data as of 7/1/16

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

1yrs 2yrs 3yrs 4yrs 5yrs 6yrs 7yrs 8yrs 9yrs 10yrs 11yrs 12yrs 13yrs 14yrs 15yrs 16yrs 17yrs 18yrs 19yrs 20yrs

InterestRate

LengthofBorrowing

COMPARING CALIFORNIA'S BORROWING COSTS TO AAA-RATED ISSUER

(as of 7/1/2016)

DIFFERENTIAL

AAA ISSUER

CALIFORNIA

For each $1.0 billion borrowed,

California would pay $17.2 million more

over a 20-year period than a AAA-rated

issuer paid.

5

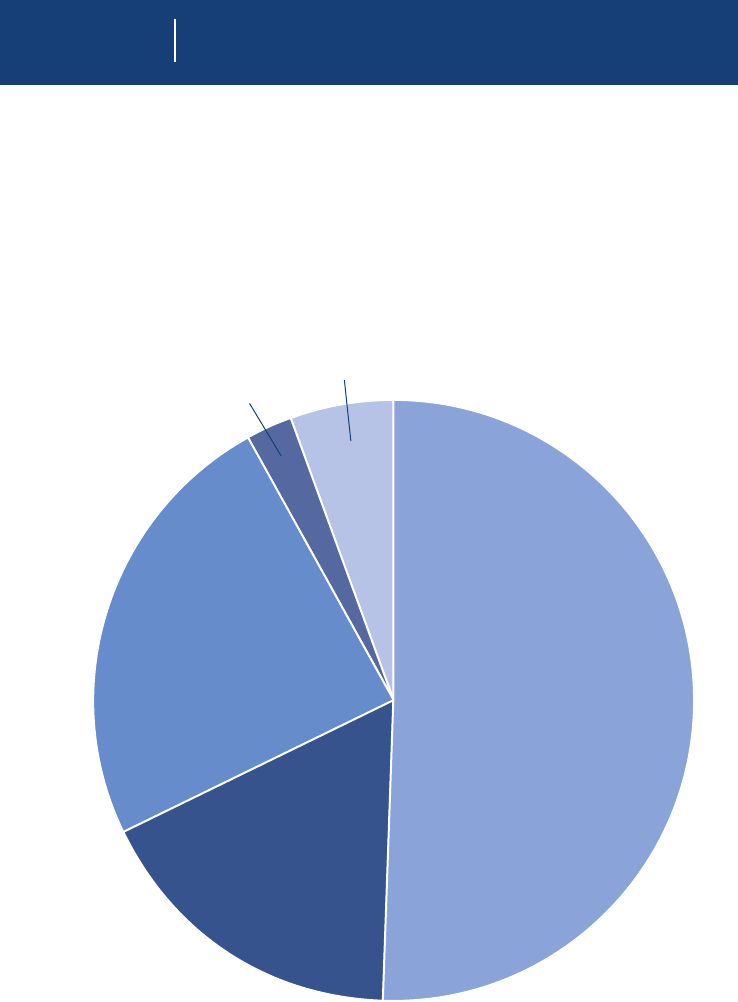

State of California’s Long-Term General Obligation Bonds Outstanding

*As of June 30, 2016

A breakdown of how proceeds of the state’s $74.9 Billion*

in outstanding long-term general obligation bonds were used:

SECTION 3 DEBT: WHAT IS IT USED FOR?

K-12 and Higher Education

$38.1 Billion

Transportation

and Clean Air

$17.9 Billion

Clean Water

and Disaster

Preparation

$13.1 Billion

Other

$4.1 Billion

Housing

$1.7 Billion

6

SECTION 4 MEASURING CALIFORNIA’S

DEBT BURDEN

Measuring California’s debt level using various ratios provides a way to

compare and understand the state’s debt burden for tax supported and general

obligation debt. ree commonly used rations are: debt as a percentage of the

state’s GDP; debt as percentage of personal income; and debt per capita.

(Figure compares what an issuer, in this

case the State of California, owes versus

what it produces. Figures as of end of

calendar year 2014.)

(Figure is based on level of debt to the

total personal income of its residents.

Personal income includes wages, business

income, interest and dividends and

governmental transfers like Social Security.)

(Figure is based on residents’ average share

of state’s total outstanding debt.)

Debt Per Capita*

Debt as Percentage

of Personal Income*

4.7%

Debt as Percentage of State GDP*

3.94%

$2,323

*Figures as reported by Moody’s in its 2016 State Debt Medians Report released May 2016.

As of end of calendar year 2014.

7

STATE MOODY’S/S&P/FITCH DEBT TO PERSONAL INCOME*

Texas Aaa/AAA/AAA 0.90%

North Carolina Aaa/AAA/AAA 1.80%

Michigan Aa1/AA-/AA 1.80%

Florida Aa1/AAA/AAA 2.50%

Pennsylvania Aa3/AA-/AA- 2.50%

Ohio Aa1/AA+/AA+ 2.60%

Georgia Aaa/AAA/AAA 2.70%

California Aa3/AA-/AA- 4.70%

Illinois Baa2/BBB+/BBB+ 5.20%

New York Aa1/AA+/AA+ 5.40%

Moody’s Median All States 2.50%

Median for the 10 Most Populous States 2.55%

STATE MOODY’S/S&P/FITCH DEBT TO CAPITA*

Texas Aaa/AAA/AAA $383

North Carolina Aaa/AAA/AAA $721

Michigan Aa1/AA-/AA $719

Georgia Aaa/AAA/AAA $1,029

Florida Aa1/AAA/AAA $1,038

Ohio Aa1/AA+/AA+ $1,091

Pennsylvania Aa3/AA-/AA- $1,172

California Aa3/AA-/AA- $2,323

Illinois Baa2/BBB+/BBB+ $2,522

New York Aa1/AA+/AA+ $3,021

Moody’s Median All States $1,025

Median for the10 Most Populous States $1,065

STATE MOODY’S/S&P/FITCH DEBT AS % OF STATE GDP*

Texas Aaa/AAA/AAA 0.64%

North Carolina Aaa/AAA/AAA 1.50%

Michigan Aa1/AA-/AA 1.59%

Ohio Aa1/AA+/AA+ 2.20%

Georgia Aaa/AAA/AAA 2.21%

Pennsylvania Aa3/AA-/AA- 2.28%

Florida Aa1/AAA/AAA 2.51%

California Aa3/AA-/AA- 3.94%

New York Aa1/AA+/AA+ 4.29%

Illinois Baa2/BBB+/BBB+ 4.41%

Moody’s Median All States 2.21%

Median for the10 Most Populous States 2.25%

*Moody’s, S&P and Fitch ratings as of August 2016.

Here’s How California Ranks Among the 10 Most Populous States

Debt to Personal IncomeDebt to Capita

Debt As % of GDP

8

*2016-17 General Fund Expenditures

SECTION 5 DEBT BURDEN COMPARED TO

BUDGETARY REVENUES & SPENDING

Other useful ways to measure debt burden is to compare it against

General Fund revenues and other budgetary spending.

Debt Service Payments

$7.7

BILLION

$51

BILLION

K-12 Education

$14

BILLION

Higher Education

$11

BILLION

Public Safety

Health and Human

Services

$33

BILLION

(Figure is based on $7.7 billion in debt

service payments versus $117 billion of

General Fund revenues in 2015-16.)

Debt Service as Percentage

of General Fund Revenues

6.54%

*

*

*

*

Debt Service Vs. Other Budgetary Spending

9

SECTION 6 CALIFORNIA REFINANCING:

HOW MUCH HAS BEEN SAVED

In Savings from Bond Refinancings Conducted

by Treasurer Chiang since January 2015*

Incoming Freshmen at University of California

Campuses for 2016-2017**

$4.2 Billion

311,111

THAT COULD PAY TUITION AND FEES FOR ONE YEAR FOR APPROXIMATELY

SAVINGS DUE TO DEBT

REFINANCINGS SINCE

JANUARY 2015

Lease

Revenue Bond

Savings -

$200 Million

Just as a homeowner can renance his or her mortgage when interest rates fall,

the Treasurer renances portions of the state debt in a similar way in order to

reduce costs to taxpayers.

*As of September 1, 2016

**Based on the average tuition and fees ($13,500) for the 2016-17 school year at UC campuses.

All other

Savings -

$1.9 billion

GO Bond

Savings:

$2.1 Billion

10

SECTION 7 CALIFORNIA’S BOND

CALENDAR

California’s general obligation bond sales generally take place three to four times

a year, generally two sales each during the respective three to four months after the

governor’s January budget release and after a budget is approved and signed in June.

California State Treasurer Chiang Sells:

$2.7

Billion in Bonds

AUGUST 2016

$1.5

Billion in Bonds

APRIL 2016

$2.9

Billion in Bonds

MARCH 2016

JOHN CHIANG | CALIFORNIA STATE TREASURER

915 Capitol Mall, Room 110

Sacramento, California 95814

(916) 653-2995

WWW.TREASURER.CA.GOV

For more information on California’s debt investment,

visit the Treasurer’s award-winning DebtWatch website

debtwatch.treasurer.ca.gov